Alternative Payment Methods Enable International Purchases

Summary: By understanding customers’ payment preferences and offering options that people are used to in their own country, sites can improve the checkout experience for international purchasers.

If you have an ecommerce site, when was the last time your team reevaluated the payment methods you offer your customers? Given how much effort goes into creating a good ecommerce experience (we have 13 volumes about it), it’s surprising to see that at the very moment when customers are ready to pay, some aren’t given a chance, because their preferred payment method isn’t an option. In particular, crossborder ecommerce sites that sell to international users must understand their customers’ expectations and preferences around payment methods in order to get their business.

In ecommerce, an alternative payment method refers to any form of payment other than a credit card. They’re called alternative methods, because on a global scale, they aren’t as popular or common as credit cards, which have been the default method in many countries, for many years. In this article, we’ll present some popular alternative payment methods and tips for how to improve the UX of selecting an alternative payment method.

The findings and recommendations here come from research we conducted for the fourth edition of our ecommerce report on international purchasers. That research included participants in China, Chile, Mexico, and Spain who were asked to use international and domestic websites.

Why Doesn’t Everyone Pay with Credit Cards?

In the United States, paying with credit card is so commonplace that it’s easy to take it for granted. Around the world, however, there are different social, financial, and convenience factors that contribute to people’s payment preferences. It’s a common refrain in our line of work: UX without users is not UX. If you want to grow your customer base, you’ve got to understand why some people choose alternative payment methods. Below are three common reasons why some people don’t use credit cards for online shopping:

Mistrust of banking institutions and credit cards. Often, people don’t trust banks and credit cards because of past personal or national events that led to problems for consumers. For example, our mistrusting users recalled instances of friends or family going into debt, having to pay unreasonable fees, or struggling to cancel unwanted credit cards. Sometimes the mistrust was rooted in government-level failures, such as a lack of consumer protection or radical financial controls (for example, the infamous “corralito” in Argentina in 2001, which froze all bank accounts for a period).

Ineligibility for banking products. In some cases, credit cards aren’t available to consumers— for example, because their income isn’t high enough or they don’t have a traditional employment contract. Young adults and low-income consumers in emerging economies are often in this situation.

Preference for convenient, mobile payments. The combination of the previous two factors with the timing of the arrival of mobile phones has led to explosive growth in mobile payments. In China, in particular, 65% of ecommerce spending in 2017 was with mobile wallets, according to a 2018 report by Worldpay. Mobile digital wallets (or eWallets) like Alipay, WeChat Pay, and PayPal can be preloaded with funds or connected directly to a bank account. They save users from carrying a physical card and manually entering payment information.

Common Alternative Payment Methods

Around the globe, there are scores of payment methods people use. In ecommerce, they generally can be grouped into a few main categories. Consider which, if any, of these may appeal to your customers.

Bank transfer. While bank transfers used to take days and seemingly a lot of work to set up (and, in the U.S., consumers rarely if ever transfer money for casual use), online banking has improved, and transfers are fast and easy in many parts of the world. For example, in many countries in Latin America, payment via direct bank transfer is so common that friends transfer money to each other as routinely as people in the U.S. use Venmo to split a restaurant bill. In addition to several countries in Latin America, bank transfer is a common and expected way to pay in the Netherlands, India, Thailand, and Poland.

For example, on MercadoLibre.com, shoppers in Mexico have the option to choose electronic transfer at checkout. They select their bank and are provided with the instructions to make the transfer on their bank’s site.

MercadoLibre.com.mx allowed users to pay via bank transfer. Users selected their bank and made the transfer from their bank’s website.

Debit cards. In the U.S., credit and debit cards are accepted online interchangeably, as long as they are branded by the major card companies (Visa or Mastercard). But elsewhere in the world, banks distinguish between credit and debit cards, so ecommerce sites require users to specify the type of card that they will use. Users trying to purchase with a debit card on a site that does not differentiate between them may have trouble, because their local bank won’t be able to complete the transaction.

Mobile-payment applications. In China, at the time of our study, mobile-payment applications like Alipay and WeChat Pay were used more than credit cards for ecommerce purchases. (And they were even popular for in-person purchases: just over one third of point-of-sale spending was with mobile-payment apps in 2017). In the example below, a desktop user logged in to Sasa.com with her Alipay account by using her phone to scan a QR code displayed on Sasa’s webpage. Once her credentials were identified, she completed the purchase from her phone.

Sasa.com: Chinese shoppers who began browsing on desktop often logged in to mobile-payment accounts, such as AliPay shown above, to complete a purchase from their phone.

In-person payments for online purchases. In some countries, like Mexico and Brazil, it’s common for people to make a purchase online and pay in person for it at a convenience store. A shopper in Mexico explained, “At Oxxo you pay your energy bill, your water bill, your bank, you can do everything at Oxxo. It’s part of the culture, so paying there isn’t a barrier.”

The Purchase Summary page on Bestbuy.com.mx offered Oxxo and PayPal as alternative payments. Choosing Oxxo led users to a page with instructions and a barcode, which could be presented to the cashier to complete the payment. (For the sake of clarity, these screenshots were translated from the original using Google Translate.)

Debit cards requiring a physical device for two-factor authentication. In Chile, consumers who want to pay with their debit card must carry around a special key fob, also known as a “disconnected token” that generates one-time passwords, which users then manually input into a website’s checkout flow to complete the purchase. While secure, this method has several downsides. First, people must remember to carry their device with them at all times if they want to make a purchase. Second, the passwords time out after 30 seconds, so users must be quick to type in the password on the screen. If the password on the device changes before the user submits the payment, the user will have to resubmit the form with a new password.

This approach also creates an additional step at checkout. Users are redirected from the original website to their bank’s payment-verification page, before returning to the original site for confirmation.

Scotiabank Chile required users to verify every online purchase by entering a code from a physical key fob into a form on the bank’s website. The device generated a temporary numeric password which had to be input on the website before it reset, after about 30 seconds.

3 Ways to Improve Payment Method UX for International Purchasers

Offer at least one alternative to credit cards. Ecommerce sites should always offer credit cards as a payment option, but this option should not be the only one. Allow shoppers to pay using another method, such as debit card, bank/wire transfer, eWallets (PayPal, Amazon Pay), or mobile-payment services such as Apple Pay, Google Wallet, Alipay, or WeChat Pay — according to what makes sense for your customers.

In some cases, the payment method can offer a competitive advantage. For instance, the password manager 1Password only offered credit cards as a payment method, while a competitor, Dashlane, accepted PayPal in addition to credit cards. In both cases, the sites were available in 10 or more languages, so it’s clear the companies are interested in selling to international customers.

1password.com only allowed users to pay via credit card.Dashlane.com allowed users to pay via credit card or PayPal, thus supporting a wider range of customers.

For country-specific sites, localize your alternative payment methods. Research the payment methods common in your target countries. Then, evaluate if it’s feasible to offer them on your country-specific sites. Include only the methods that are likely to be popular with your audience.

For example, the Walmart website offered different payment options in Brazil and the United States. In the United States, there were 8 ways to pay. But in Brazil, Walmart.com.br offered just 3 options: credit card, debit card, and bank ticket.

Walmart’s Brazil site tailored the payment options to fit what was expected in that country: credit card, debit card, and cash/bank ticket. (For the sake of clarity, this screenshot was translated from the original Portuguese using Google Translate.)

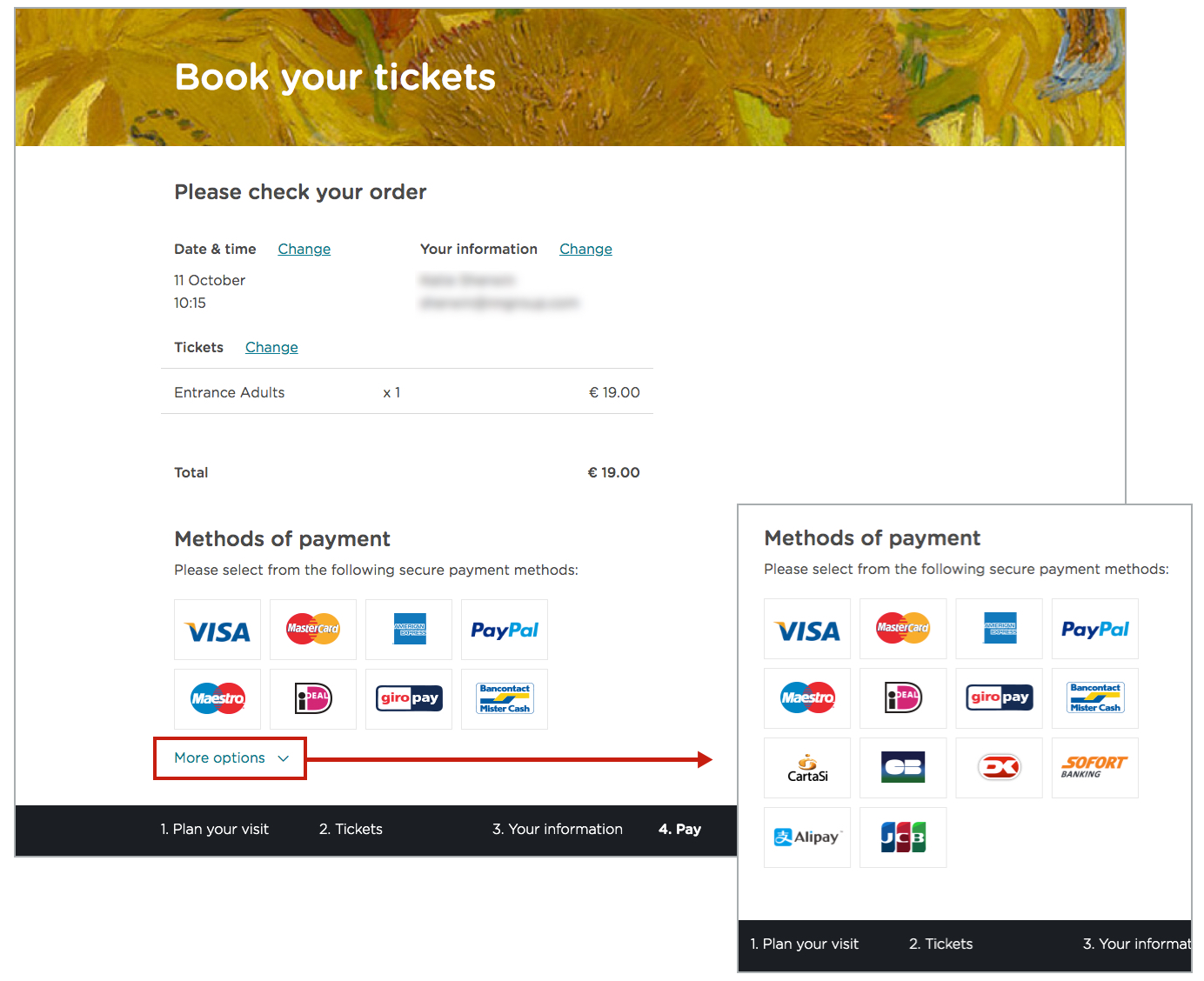

In the Netherlands, the Van Gogh Museum offered 8 payment methods visible by default, including popular payment choices in the Netherlands (iDeal), Germany (giropay), and Belgium (Bancontact). Customers could view More options and see an additional 6 ways to pay. If you’re thinking 14 methods sounds like choice overload, you might be right; in many instances more is not better. However, given the museum’s status as an international attraction, it’s appropriate that this site welcomed a diverse range of payment methods.

Vangoghmuseum.com offered 14 payment methods to accommodate the variety of international visitors that buy tickets for the museum.

In addition to considering eWallets and bank transfers, it’s normal in many places around the world to pay in installments (particularly for expensive items like appliances, electronics, and jewelry), and that approach is becoming more common in the United States as well. Evaluate whether including a payment-plan method, such as Klarna or Affirm, would appeal to your customers.

Consider the quality of the checkout experience for those users who must take additional steps to make a purchase. For example, users who opt to pay in person (via Oxxo or Boleto Bancario, for example) should be able to easily access the deposit details: the site could send the information via email or text message or might present it in a printable format. Or, customers who must use an external security token should be able to go through the checkout as smoothly and quickly as possible, without any additional steps or upsell screens, to compensate for the extra work involved in using the one-time password.

Conclusion

If people from other countries already visit your site and make purchases, you might think it isn’t necessary to adjust your payment methods for them. But you’d be wrong. For each international customer that makes a purchase, there could be others who abandon checkout because they aren’t comfortable with any of the options available.

If your online sales are low in a particular country, conduct research and examine your analytics data to explore whether inadequate payment options could be the reason. Companies aiming to grow their international-customer base should start with the most-popular payment methods in those countries which already provide them with visitors and track the results after implementing the changes.

Katie Sherwin is a Senior User Experience Specialist with Nielsen Norman Group. She specializes in helping organizations utilize principles of user-centered design and strategic communication to achieve their goals.

Subscribe to our Alertbox E-Mail Newsletter:

The latest articles about interface usability, website design, and UX research from the Nielsen Norman Group.

Share this article: